Monitoring your credit report frequently is a smart practise since improving your credit score takes time. Nevertheless, watching your credit report frequently will also assist you in recognising identity theft sooner.

Indian borrowers are becoming more aware of the importance of monitoring their credit record and score. According to a TransUnion CIBIL study, 23.8 million customers signed up with the company in 2022 to check their credit profiles for the very first time. This was 83% more people than had subscribed in 2021.

Monitor your credit score often:

Get a copy of your credit profile at least once every three months. To make sure you are always credit-ready, keep an eye on your credit record frequently, not just when you need a loan.

Regularly reviewing your credit report will alert you to a number of problems. Identity fraud is one. It is possible that a scammer could have obtained a loan using your identity. Only via routine monitoring will you be able to identify this issue early and notify the authority, the bank, and the credit agencies.

A borrower could believe his credit score is high. Yet he could find out it’s merely mediocre when he applies for the loan. He might have improved his report if he had been paying close attention to it. A lender’s decision to approve a loan request and the rate of interest it charges depends on the borrower’s credit score. It might take two to three quarters or more to raise the score, depending on the starting point. You can become aware of mistakes you’ve made and problems with the lender’s procedures by keeping an eye on your credit report. You could have forgotten to make a payment that you are unaware of. It’s possible that a payment you made didn’t go through or that its execution took longer than expected.

Consider doing the following 5 checks:

1. Verify your credit score. If it is high, you can be sure that you will always be able to acquire a loan at a competitive rate. If it’s mediocre or poor, try to make it better.

2. Review the history of all debts taken out and repaid. Occasionally individuals make errors. A different person’s credit activity might be represented in your account.

3. Verify that your credentials such as name, date of birth, address, PAN number, and other information have been accurately logged.

4. Review the section on enquiries. Every time you ask for a loan, the lender checks your credit history. So this data gets reflected in the enquiries section of the portal. If an enquiry is made known but you haven’t applied, it should be taken as a sign that someone is attempting to exploit your credit record.

5. Compare the principal balance for each debt included in your credit report to the information that you have in your records. If there is a disparity, it can indicate that the interest rate has increased, a penalty has been assessed, or some other matter that needs to be investigated.

How to take remedial action:

Make sure your credit report is repaired if you find an error. Work together with the lender and the credit agencies to make the correction.

If your report indicates that you have not made a payment, make the repayment as soon as possible.

Keep in mind that your payment history accounts for 35–40% of your credit score.

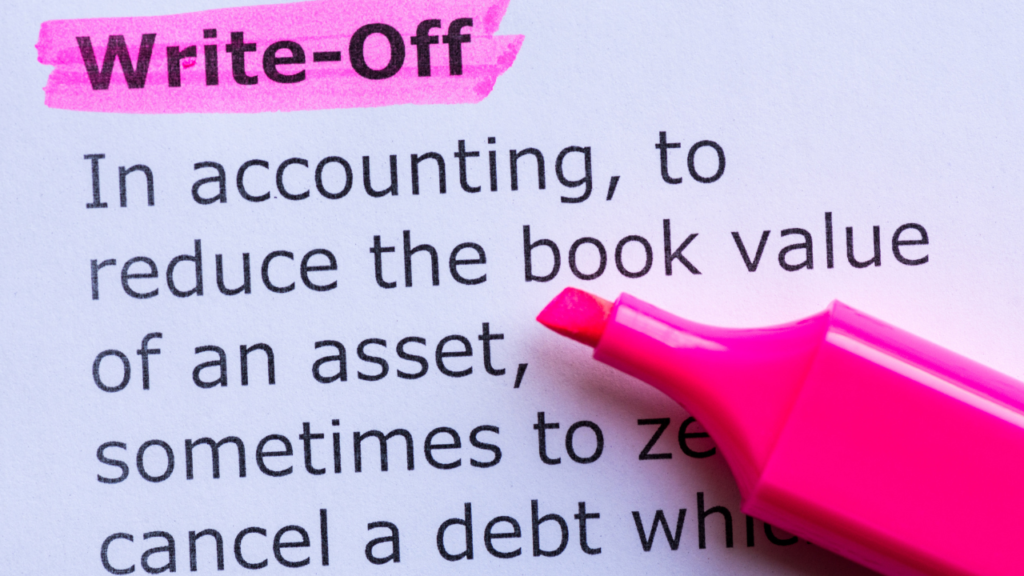

You can owe fees that you haven’t paid in more than 90 days. This type of loan account is referred to as a “write off.” Ensure the “write off” marker is eliminated from your credit report after you’ve paid the outstanding balance.

Another possible term in your report is “settlement.” Lenders may make settlement offers when a borrower is unable to pay their debt in full. It can agree to settle the account for Rs. 70 rather than the required Rs.100. Such a compromise, nevertheless, lowers your rating. Make the debt payment entirely to get the settlement label off of your credit record if you wish to enhance your credit score.