Inflation means that over time the prices for everyday goods and services tend to rise. This steady increase makes each unit of money worth a little less than before, so your cash buys fewer items as time goes on. In simple terms, when inflation goes up, the same sum of money will not get you as much as it once did. This blogpost is intended to help you grasp the basic concepts of inflation and its effects on investments in an easy-to-understand manner.

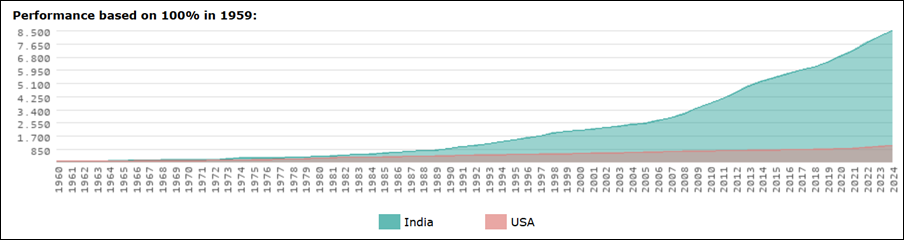

Over many decades in India, from 1960 to 2024, the average yearly inflation rate has been about 7.3%. This means that prices increased so much that something costing 100 rupees in 1960 would cost roughly 8,471 rupees by early 2025. Although the number 100 stays the same nominally, its power to buy goods shrinks significantly over time. In the recent year 2024, the inflation rate was measured at 4.4%, with December 2024 showing a year-over-year rise of 3.53%.

Source: IMF and World Bank.

If we look at a shorter span, such as the last five years up to the end of 2024, the annual inflation rate averaged around 5.6%, adding up to a total increase of about 31.5%. In comparison, the United States experienced an average of 4.2% per year and a cumulative increase of 22.7% over the same period. These differences remind us that inflation can vary widely by country and period, influencing economic decisions differently.

Table of Contents

Inflation’s Effects on Investments and the Economy

Inflation does more than just change the price of bread and milk, it also affects how your investments perform. When inflation is high, the actual value of your savings and investments declines in real terms because the money you receive later does not have the same buying power as before. To counter the loss of value, central banks often raise interest rates.

For example, the Reserve Bank of India (RBI) may increase interest rates to slow down an overheated economy and to manage price increases. These rate hikes usually have a negative impact on stock markets, as higher borrowing costs and lower profit margins tend to hurt companies. Conversely, when inflation falls and prices stabilize, central banks might lower rates, which can boost the market and encourage investment in stocks.

There is also an important link between inflation and market valuation. Investors typically adjust the prices they are willing to pay for stocks based on the inflation rate. A common guideline suggests that if the overall price-earnings ratio for stocks exceeds “20 minus the inflation rate,” the market might be considered overvalued. For instance, with an expected inflation rate around 5% for 2024, a fair multiple for evaluating major stock indices would be near 15 times expected earnings. Despite such benchmarks, some indexes might still trade higher due to a few very large companies pushing the averages upward.

When it comes to bonds, investors compare the bond’s interest rate with the inflation rate. If a bond does not offer a rate higher than inflation, its real return might be negative. Therefore, when planning investments in bonds, it is crucial to consider what the inflation trends suggest for the future. Essentially, the key to investing wisely is to manage expectations about inflation over the life of the investment.

Different Economic Environments: A Closer Look

Economists have identified several “pricing environments” that describe how prices behave in an economy. Each type of environment has different implications for investments and requires a tailored approach. The main categories are inflation, disinflation, no-flation, deflation, and stagflation, and we will look into each of these categories in-detail below.

1. Periods of Inflation

A moderate level of inflation is normal in a growing economy. In fact, a small, steady rise in prices can encourage spending and investment. However, if inflation climbs above about 2% annually, it might start causing concern among policymakers, bankers, and business owners. In such cases, companies may be forced to raise their own prices to keep up with rising costs, and employees may demand higher wages. This can create a cycle that pushes inflation even higher.

During these times, certain investments tend to do better because they help protect against the loss of purchasing power. For example, gold is often considered a safe bet because its value tends to increase when currency values drop. Other popular options include real estate, since property values and rental incomes often rise with inflation, and stocks from companies that are able to transfer higher costs to their customers. Investments in commodities, such as oil and agricultural products, can also benefit as their prices tend to increase during inflationary periods. Additionally, some government-issued bonds have interest payments that are adjusted for inflation, helping investors maintain their real returns over time.

2. Periods of Disinflation

Disinflation happens when the rate at which prices are rising starts to slow down. Even though prices continue to go up, the pace of their increase is lower than before. This slowdown can be good news for the economy because it often means that companies can manage their costs better and generate higher profits. As a result, stock markets might see a boost since investors tend to favor businesses that have stable and improving earnings.

In a disinflationary period, growth-focused companies, particularly those in sectors like technology, finance, and consumer products, might perform well. Bonds purchased during previous high-inflation times might now deliver better real returns because the rate of inflation is easing. With lower inflation, central banks are more likely to reduce interest rates, which further encourages borrowing and investing. However, investments such as commodities might suffer because lower inflation usually means less upward pressure on their prices.

3. Times of Price Stability (“No-Flation”)

When an economy experiences very little inflation—typically defined as an annual price increase of no more than 2%, it is often considered to be in a “no-flation” phase. This stable environment is seen by many investors as a golden period because predictable prices support steady earnings for companies. Industries like consumer goods, healthcare, utilities, and technology generally do well because the demand for their products does not waver much in such times.

The calm of price stability also benefits fixed-income investments like government bonds and corporate bonds, which offer consistent returns. Investors might even find that riskier investments, such as small company stocks or growth stocks, become more attractive because the stable economic environment reduces uncertainty. With inflation remaining low, companies have an easier time planning for the future, and this predictability can lead to improved profitability and growth.

4. When Prices Fall: Deflation

Deflation is the opposite of inflation; it happens when the overall price level starts to drop over time. While lower prices might sound like a benefit at first, deflation is usually a sign of a weak economy. Falling prices can lead to reduced demand because consumers might delay purchases in the hope that prices will fall further. This delay causes companies to earn less revenue, which can result in lower wages, job losses, and overall economic slowdown.

In a deflationary environment, safe and secure investments become more important. Instruments such as government bonds, fixed deposits, and short-term debt funds tend to perform well because they offer steady returns and low risk. Additionally, holding cash can be advantageous since its value increases in real terms when prices drop. For companies, only those with strong financial foundations and low debt are likely to withstand the downward pressure. Investors are generally advised to avoid taking on new debt during deflation since the real burden of any existing debt increases as prices fall.

5. The Challenge of Stagflation

Stagflation is a particularly difficult economic situation where high inflation and a sluggish economy occur at the same time. In such a scenario, the economy experiences both rising prices and slow or no growth, which creates significant challenges for investors. High inflation reduces the value of money, while the stagnant economic environment limits the ability of companies to increase their profits. This combination can make it hard for traditional investments like stocks and bonds to deliver good returns.

During stagflation, precious metals such as gold and silver often gain appeal because they tend to hold their value even when inflation is high. In addition, investments in commodities like oil, natural gas, and agricultural products may benefit from persistent price pressures. Certain sectors that produce essential items—such as consumer staples, healthcare, and utilities, can also be more resilient during these tough times because they offer goods and services that people continue to need regardless of economic conditions. For those exposed to local economic challenges, diversifying investments internationally may help balance the risks posed by stagflation.

Strategies for Managing Inflation in your Investment Portfolio

Given the many ways that inflation can impact your money, it is important to adapt your investment strategy accordingly. Here are some key points to consider:

- Diversify your Investments: Spread your money across different asset classes such as stocks, bonds, real estate, commodities, and precious metals. This mix can help balance the risks associated with rising prices.

- Focus on Inflation-Resistant Assets: Consider investments like gold, real estate, and inflation-indexed bonds, which are designed to protect your purchasing power when prices increase.

- Stay Informed About Economic Trends: Keep an eye on inflation statistics and central bank policies. Being aware of changes in the economic environment can help you make timely adjustments to your portfolio.

- Consider the Time Horizon: While stocks may be volatile in the short run during inflationary periods, they often offer strong protection over the long term if you are willing to hold them for five years or more.

- Watch Your Debt: When inflation is falling or in a deflationary phase, it becomes more important to manage your debt carefully, as the real value of any outstanding loans can increase.

Final Thoughts

Inflation is an inevitable part of economic life, but understanding how it works can help you make smarter financial decisions. By knowing how inflation has affected prices historically and how it influences different types of investments, you can plan for a range of economic environments. Whether you are looking at protecting your savings or trying to grow your portfolio, staying informed and diversifying your investments are key strategies for success.

The ideas presented above in this blogpost give you a clear, comprehensive picture of how inflation affects both the everyday cost of living and your long-term financial planning. With this understanding, you will be better equipped to navigate the complexities of inflation, economy and make decisions that protect and grow your financial resources over time.

You can also check out my other article on five important money tips to Stay Ahead of Inflation.

Do Follow me on Linkedin and Quora for more such insightful posts on personal finance, money management, investments, retirement, etc.