When markets reach all-time highs or at all-time lows, the age-old debate about valuation reignites. However, before you consider changing your investment allocation based on whether the market looks to be overpriced or undervalued, you must first understand which valuation criteria are important. The price-earnings (PE) ratio is one such statistic that might help solve this complex conundrum. The PE ratio is a financial measure that reduces to a simple equation: It divides the current market price of a stock, which reflects the amount you are prepared to pay to purchase it, by the earnings per share (EPS), which corresponds to the earnings generated by each share that you own.

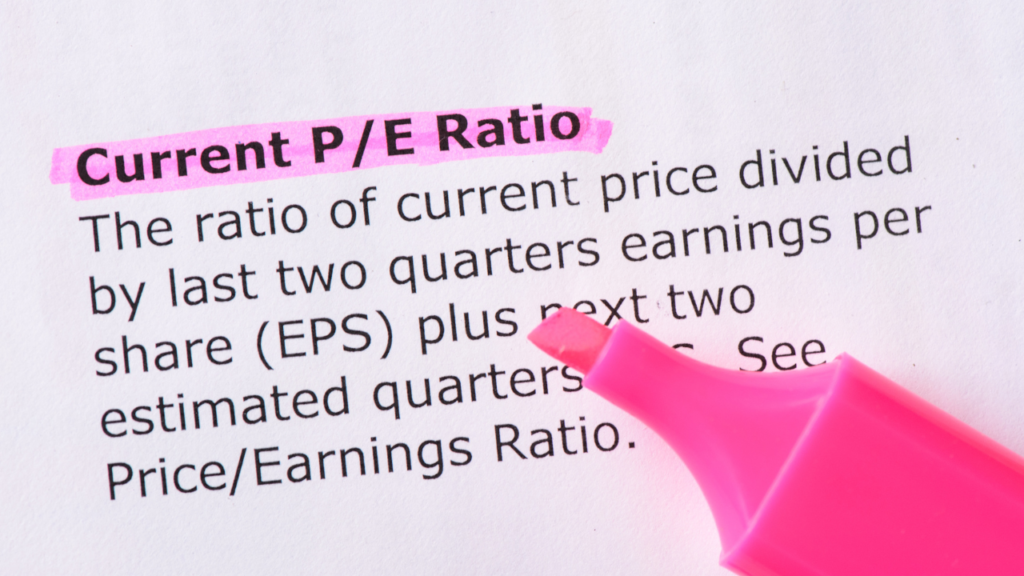

In simple terms, the PE ratio is the price you are willing to pay for a company’s yearly earnings. For example, if a stock has a PE ratio of 15 times, it means that for every one rupee earned by that company, you are prepared to invest 15 rupees in that company. However, it is important to realize that this pricing does not represent just real earnings. Rather, it indicates your expectations for the company’s yearly profits growth. A high PE ratio suggests that profits growth will be strong in the future year, whilst a low PE reflects a more conservative perspective. As an investor, you must understand the two primary versions of the PE ratio: trailing PE and forward PE.

The trailing or historical PE is calculated using earnings data from the previous 12 months, offering a glimpse at the company’s prior earnings history. The forward PE, on the other hand, is calculated using the projected one-year profits for the following fiscal year. These projections might be based on your own estimations of how the company’s earnings are likely to manifest, or they can be driven by the opinion of stock experts in the field of finance or investments. Notably, the forward PE is a more variable indicator, subject to changes induced by company press releases or external variables that may affect future earnings predictions.

Looking at PE Ratio in isolation:

When seen in isolation, the PE ratio provides insufficient information. To draw significant conclusions, multiple factors must be considered, including the sector in which it operates, its position within a larger investing portfolio, and its previous performance trends. The PE multiple is used to evaluate a stock’s attractiveness in terms of price comparative to the wider marketplace, as measured by the index’s PE ratio, as well as in comparison with similar firms by comparing it to the sector’s average PE ratio.

It is critical to understand that a stock with a low PE multiple might not always be a good investing option. This lower multiple may represent the market’s perception of the company’s restricted potential for expansion, leading to a less favorable value. In contrast, a high PE multiple must be supported by strong growth prospects in order to be regarded reasonable. In essence, the relevance of the PE ratio increases when considered in light of industry standards, market trends, and a business’s growth prospects. The foundational assumptions and their accuracy with actuality are the most important elements at play. Stock market valuations are generally (but not always) forward-looking. This means that investors are prepared to pay a present price that reflects a company’s estimated future profits growth.

Every corporation has its own valuation metrics. A company trading at a PE ratio of 10 times earnings may look pricey, whilst another may appear decently priced even at a PE ratio of 15 times. The essential factor should be a company’s ability to continuously create earnings growth while maintaining a reasonable profit margin. It is not strange to see a company selling at an elevated valuation when it continuously generates an impressive return on capital, displays long-term growth, retains an edge over its competitors, and continues on its path of growth. In this scenario, investors are ready to pay a higher premium for these firms that demonstrate long-term viability and an established history of consistent profit generation.

Shortcomings of PE ratio:

- One obvious issue of relying exclusively on the PE ratio is the implicit belief that a company’s future earnings would, at the very least, mirror its present earnings. For someone involved in the field of investment, it becomes clear that projecting a company’s profitability even a year or two ahead is a difficult undertaking, given the volatile nature of marketplaces and business climates. Trying to forecast earnings for the next ten years is an even more daunting task.

- One restriction is the belief that stocks trading at 15 times earnings are always cheaper than those trading at 20 times earnings. This common idea is based on the expectation that a firm will retain its present profit levels in the coming years, enabling investors to get back their initial investment. However, in practice, this assumption is mostly academic. The hard fact is that a company’s profits trajectory in the future years might vary greatly.

- The PE ratio does not indicate the soundness of a company’s balance sheet or its financial position. There may be cases where a firm with an apparently modest PE ratio of only 2 times earnings is nonetheless significantly costly due to an underlying issue, such as a significant amount of current debt that it lacks the ability to service. As a result of this scenario, the firm may declare bankruptcy within the current fiscal year.

- It is very common to hear talks comparing two firms, one trading at a PE of 10 times earnings and the other at 20 times earnings, and concluding that the former is the cheaper alternative. However, a more in-depth evaluation is necessary here, as there are various criteria that might have caused the lower PE of 10, such as a one-time windfall profit that is improbable to occur again. This would have increased their earnings and hence provided a lower PE in that year, but this may not be the case in subsequent years.

Final Thoughts:

A company’s intrinsic worth is evaluated by its ability to generate cash flows, instead of just earnings. Sadly, the stock market, sometimes mistakenly places a high value on earnings and PE multiples, distracting the focus away from the key component responsible for accumulating wealth, which is the cash flow of the business.

As rightly said by the legendary investor Warren Buffett, dividend yield, PE ratio, Book value, etc., are all general indicators that provide signals to the amount and timing of cash flows into and from the business. The PE ratio alone does not provide the depth required for informed decision-making to pick stocks. Warren Buffett has recognized that using the PE ratio alone to calculate a stock’s real intrinsic value might be inappropriate. Using the PE ratio as the primary metric is similar to determining a person’s weight by simply looking at their shadow.

Long-term investors should dismiss short-term changes in the PE ratio, which are frequently impacted by market volatility and liquidity considerations. Rather, make informed investing decisions based on the long-term qualities of a business’s earnings capability. While the PE ratio is still a useful tool for analyzing equities, investors should use it in combination with other valuation techniques. It should never be used as the only basis for financial choices.